Frequently Asked Questions

1. INVESTMENTS 101

Asset classes are the underlying instrument of an investment portfolio in which an investor’s capital is invested in. Asset classes can be categorised as traditional or alternative.

This is a risk management strategy that reduces overall investment risk by spreading the portfolio’s exposure between underlying assets, managers, geographies etc.

The sharpe ratio is the average return earned in excess of the risk-free rate per unit of standard deviation or risk. So if an investment returns 12% at a standard deviation of 5% and the risk-free rate was 4%, the sharpe ratio is: (12-4)/5 = 1.6

Volatility refers to fluctuations in value of an asset or portfolio. Higher fluctuations (volatility) in value are dangerous for an investor with a short-term investment horizon, because the value of the underlying asset could possibly not recover from a large drop in value in the short term. Different asset classes have different levels of volatility, therefore it’s important to allocate capital appropriately according to the invest need.

2. TRADITIONAL ASSETS

A traditional asset class consists of the following 4 asset classes: cash, bonds, property and equity.

Cash is the asset class with the lowest exposure to risk because a fixed interest rate is used. Cash as asset class is predominantly represented by money market instruments. When cash is used as an underlying asset it is important to into consideration the effect of inflation because traditionally this asset class struggles to outperform inflation over the long term. Cash can thus be seen as a short term asset class which can act as a safe haven in times of market fluctuations.

Bonds contain more risk than cash. Corporate and governmental institutions borrow capital and repay it at a fixed interest rate for a fixed time period. Capital is thus not liquid in this time period. Interest earned by the bond (the coupon) is usually higher than that of cash but is correlated to prevailing market cycles.

Property as an asset class contains more risk than fixed interest investments. An investment in property will be appropriate for investors requiring income as well as capital growth.

Equity is the asset class that has delivered the highest growth over time compared to other asset classes over the last 20 years. It also contains the highest level of risk. In an investment portfolio equity is used for capital growth but dividends are also declared by the underlying companies. This asset class is suitable for investors with an investment horizon of more than 5 years because of the inherent volatility of equities.

3. ALTERNATIVE ASSETS

Hedge funds aim to achieve positive returns at a reduced level of risk. Characteristics making hedge funds unique include the use of derivatives, short selling, leverage etc. to be able to extract positive performance in both upward and downward trending financial markets. Although hedge funds invest in the same asset classes as traditional unit trust funds, they can take advantage of a wide range of price adjustments and thereby generate other sources of return. Hedge Funds tend to have low correlations to traditional portfolios of stocks and bonds, therefore, allocating an exposure to hedge funds can be a good diversifier.

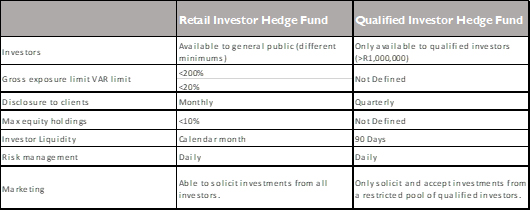

Under the new regulation, CISCA classifies hedge funds into two categories- retail investor funds(RIHF) which have more stringent regulatory requirements, and qualified investor hedge funds(QIHF)

A qualified investor, as defined by the Financial Services Board(FSCA) Board Notice 52 of 2015, is any person who invests a minimum investment amount of R1 million per hedge fund and who –

- Has demonstrable knowledge and experience in financial and business matters which would enable the investor to assess the merits and risks of a hedge fund; or

- Has appointed a Financial Services Provider (FSP) who has demonstrable knowledge and experience to advise the investor regarding the merits and risks of a hedge fund investment.

A retail investor hedge fund is defined as a hedge fund in which any investor may invest because it meets the requirements set out by the FSCA.

Some of the characteristics are tabulated below:

The buying of a security such as stock, commodity or currency, with the expectation that the asset will rise in value.

For example, an owner of shares in Stock Sasol is said to be “long Sasol” or “has a long position in stock Sasol”

For example

Buy 10 Sasol shares @ R100 per share (with the expectation that the asset will rise in value).

Total investment = R100 x 10 = R1000

The share price rises to R135 per share

Portfolio Value = R135 x 10 = R1350

Profit (when selling) = R1350 – R1000 = R1350 = R350/R35 per share

The sale of a borrowed security, commodity or currency with the expectation that the asset will fall in value.

For example, if a manager borrows and sells Stock Sasol, it is said to be “short Sasol” or “has a short position in Stock Sasol”

For example

Borrows 10 Sasol shares and sells on the open market @ R100 per share (with the expectation that the asset will fall in value).

Share price declines to R75 per share

Portfolio Value = R75 x 10 = R750

Profit (when buying back) = R1000 – R750 = R250 = R250/R25 per share

Equity long/short:

Funds aim to generate positive returns by being simultaneously long and short in the equity market. Market risk is reduced while company specific risk is retained. The majority of local equity long/short funds tend to be long biased.

An investing strategy of taking long positions in stocks that are expected to appreciate and short positions in stocks that are expected to decline. A long/short equity strategy seeks to minimize market exposure, while profiting from stock gains in the long positions and price declines in the short positions.

Equity Market Neutral:

Funds take similar sized long and short positions in related equity sectors with that effect that directional market risk is offset.

A strategy undertaken by a manager that seeks to profit from both increasing and decreasing prices. Market-neutral strategies are often attained by taking matching long and short positions in different stocks to benefit from mispricing and delivering positive returns from both the long and the short stock selections and reducing risk from movements in the broad market.

Fixed Income Arbitrage:

An investment strategy that attempts to profit from arbitrage opportunities in interest rate securities. When using a fixed-income arbitrage strategy, the investor assumes opposing positions in the market to take advantage of small price discrepancies while limiting interest rate risk.

This general strategy type includes basis (e.g. cash, futures), yield-curve and credit spread trading, as well as volatility arbitrage.

Statistical arbitrage:

Quantitative models are used to identify market opportunities and establish short-term positions involving a large number of securities.

Volatility arbitrage:

Funds aim to exploit mispricing is the result of different volatility assumptions by price makers.

Commodities:

Funds that predominantly invest in soft or hard commodities. These funds can follow a number of different strategies to obtain alpha from this asset class, including trend following or non-directional market neutral strategies.

4. WHAT TO EXPECT FROM MY INVESTMENT

It’s your investment – you decide how much, when and how you want to invest. You can add lump sums to your investment at any time. You can set up a debit order (minimum R500) at any time, which you can change, pause or cancel as your needs change. You own the units you have bought and your investment continues to earn return until you decide to sell your units.

We will send you a statement monthly showing how many units you have in your account, and what the rand value is. Alternatively, you can call Salvo at any time to get info about your investment.